2023 Week 1: Starting With A Bang!

Tesla in trouble, TikTok shaking up the digital ads space and 2023 IPO market looks gloomy

💡Did you know? Mitsubishi was one of the four largest Zaibatsus in Japan, aiding Japanese imperialism during WWII and benefitting from slave labor in conquered nations.

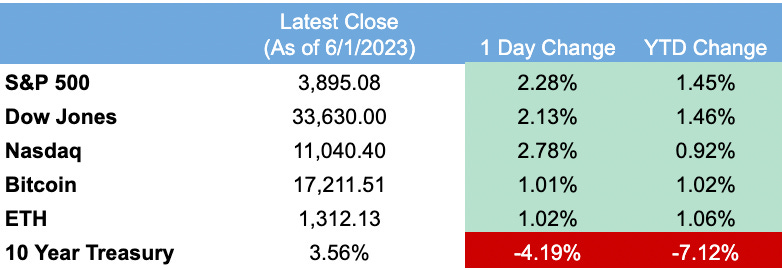

Market Summary

Tesla: Tough Road Ahead

📝A Quick Recap

Even with more discounts than usual, Tesla reported a 40% year-on-year growth in vehicle sales, falling short of its 50% growth rate ambition. Following the announcement, Tesla’s stock dropped 9% (73% from the stock’s all-time highs) to ~$108 per share.

A weaker macroeconomic outlook has been the most significant contributor to the decline in vehicle orders.

Unless they are wealthy, consumers generally do not purchase vehicles with cash. Instead, a majority borrow capital from banks to finance vehicle purchases. However, as the Fed hikes interest rates to curb inflation, borrowing funds to purchase cars is not as appealing as before.

🧐Analyze like a Consultant

Focus on maintaining margins: The automobile industry is highly correlated with the broader economy. Hence, there is little Tesla could do to boost sales in a weak economy. Tesla is already offering discounts to increase vehicle orders, but that's the most it can do to stimulate demand.

Instead, in a weak macroeconomic environment, maintaining profit margins is Tesla's logical course of action. This way, Tesla minimizes the impact on its free cash flow and builds cash reserves for potential expansion in a booming economy.

So, does Tesla have the ability to maintain its profit margins?

It is important to remember that Tesla is still an automobile company. For Tesla to maintain/reduce cost per vehicle, it can either reduce input costs and/or leverage economies of scale to spread fixed costs across many vehicles.

Wall Street is confident in Tesla's ability to maintain its vehicles’ margins, but there are a few factors that could hinder Tesla's ability to do so:

Input costs could increase: Analysts expect the Inflaton Reduction Act (IRA), which Tesla qualifies for, would lower Tesla's battery production costs, generating ~2-3% in margin improvement.

But, there is still the question of the cost of Lithium, a major component in EV batteries. The price of Lithium has skyrocketed to ~$70k/ton vs. ~$20k/ton in 2021. Further price increases will erode margins depending on the demand and supply forces.

Economies of scale: Analysts are hoping production ramp-up in Tesla's Berlin and Austin factories to drive the cost per vehicle down. But, this is grounded on the assumption that Tesla can meaningfully increase car sales in 2023 — a big assumption.

As mentioned previously, US vehicle demand is already on the decline. Making matters worse, only 10-20% of Tesla's vehicles (vs. analysts' assumption of 60-70%Tesla vehicles) now qualify for the revamped EV sales credits. In other words, the number of customers eligible for tax credits is even lower than previously forecasted, further dampening Tesla's demand.

These recent developments dent Tesla’s ambition to lower the cost per vehicle with a production ramp-up in new Giga factories.

🤷♂️What does it mean for an investor?

As the economy heads into a recessionary territory, investors are more concerned with firms' profit margins than their growth. As for Tesla, investors expect the firm to maintain its margins more effectively than its competitors, justifying the valuation premium they assign to the firm vs. its competitors -- bad news for Tesla.

There is a possibility that Tesla's market cap will plunge further in 2023 as the firm experiences pressure to maintain its margins. Only time will tell.

Digital AD Sector Experiences A Shake Up

📝A Quick Recap

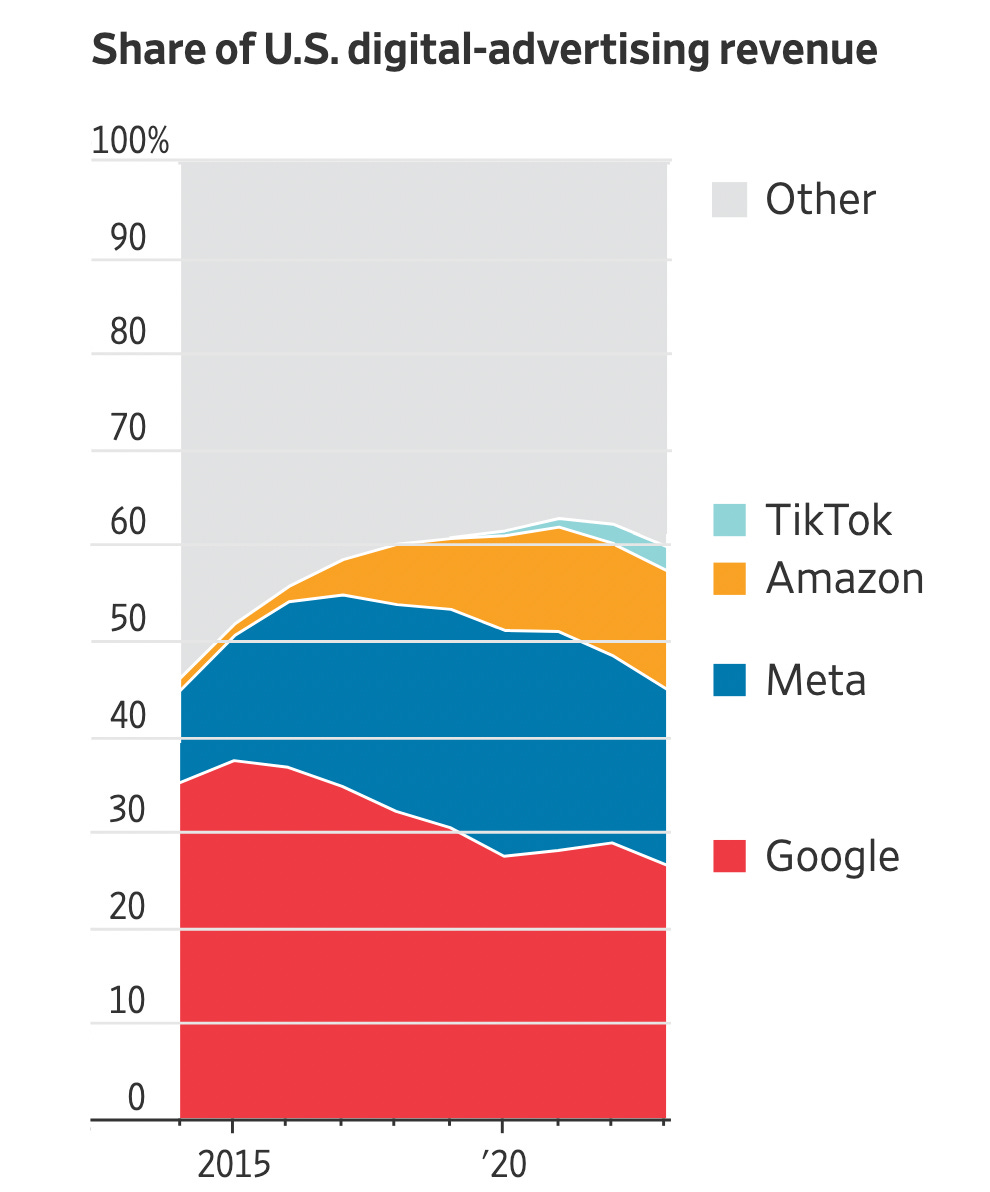

Meta and Google account for 48.4% of the US digital advertising market share (their share has never declined below 50% since 2014). Why?

TikTok and Amazon are rapidly taking market share from the incumbents as the number of users grows on these platforms. Making matters worse, video streaming platforms (e.g., Netflix, Disney +) are also launching their ad services, further intensifying competition in a crowded digital ad space.

🧐Analyze like a Consultant

Let's consider this phenomenon from Meta's perspective, the biggest loser from TikTok's and Amazon's emergence.

If you are Zuckerberg, you only have five options:

Do Nothing — a perfect recipe for disaster.

Acquire TikTok/Other Players — impossible given anti-trust scrutiny over Meta, and Meta lacks the market cap (lost 75% of its value in 2022) to buy competitors

Copy TikTok — already underway with Insta and FB Reels.

Strengthen core offering — is there room for improvement?

Building something revolutionary — already building the metaverse, which has been underwhelming. Is there another avenue to create something novel? A question for the Meta team to ponder upon.

Copy TikTok: FB and IG Reels' engagement is rapidly increasing, yet the Reels' monetization lags behind Feed and Stories. To overcome this issue, Meta has invested in improving Reel content discovery and recommendation capabilities and has launched varying Reels ad formats to lower barriers to advertising on Reels.

Nevertheless, as an investor/individual interested in buying Meta's stock, one should monitor the return on Meta's efforts to bolster its Reel Ads. What metrics to focus on in the upcoming earning calls?

Check if Reel ads’ uptake has increased (e.g., improvement in Reels' annual run rate and cost per impression)

Check for increased user engagement levels (e.g., improvement in minutes spent per day on Reels)

Strengthen core offerings: Messenger (IG and FB) and WhatsApp are Meta's competitive moats — ~4 billion users. No player globally is a threat to Meta in the messaging space. So, why not double down on this competitive advantage?

In fact, Meta has made some progress in monetizing its messaging services via click-to-messaging ads. They show great promise. Click-to-messaging ads on FB and WhatsApp have a $9 billion annual run rate, collectively contributing to a ~10% upside to Meta's overall revenues.

What should investors look out for as Meta grows its click-to-messaging ads in 2023?

Click-to-messaging ads' uptake in developing markets where WhatsApp and FB messenger penetration is high

If growth is disappointing in these markets, then scaling the product in developed markets will be more difficult.

Cannibalization of revenues from other Ad products (e.g., stories, feed)

Do advertisers view the click-to-messaging ads as a complement or substitute to stories and feed ads?

IPO Drying Up

📝 Quick Recap

Following the IPO frenzy during the pandemic (when raising capital was cheap), the appetite for an IPO has drastically decreased in 2022. 2023 is going to be no different. The IPO pipeline is dry, and investors do not expect the market to recover at least until H2 of 2023.

Contributing factors:

High-interest rates increase the cost the capital, which negatively affects the valuation

Uncertainty over the macroeconomic outlook adds volatility to the markets and decreases investors’ appetite to fund growth companies (aka newly IPO’d firms)

Companies that had IPO’d during the pandemic have experienced drastic losses in share price, deterring investors from funding IPOs

🗒Weekly Headline Summary

Asia-Specific

NY Fed says China's COVID woes are pressuring supply chains|RT

Asia stocks on track to enter bull market on China optimism, Fed rate bets|Strait Times

Chinese Semiconductor IPOs Surge as Chip Arms Race Heats Up|WSJ

Jakarta-based fintech Akulaku raises $200M from Japan’s largest bank|TC

Beyond Asia

Putin bans Russian oil exports to countries that implement price cap|RT

Signs of Seller Exhaustion Left Stocks Primed for a Big Bounce|BB

AmerisourceBergen Hit With Federal Lawsuit Over Opioid Crisis|WSJ

Southwest Resumes Normal Flight Schedule After Mass Cancellations Stranded Travelers|WSJ

SpaceX raising $750 million at a $137 billion valuation, investors include Andreessen-Horowitz|CNBC